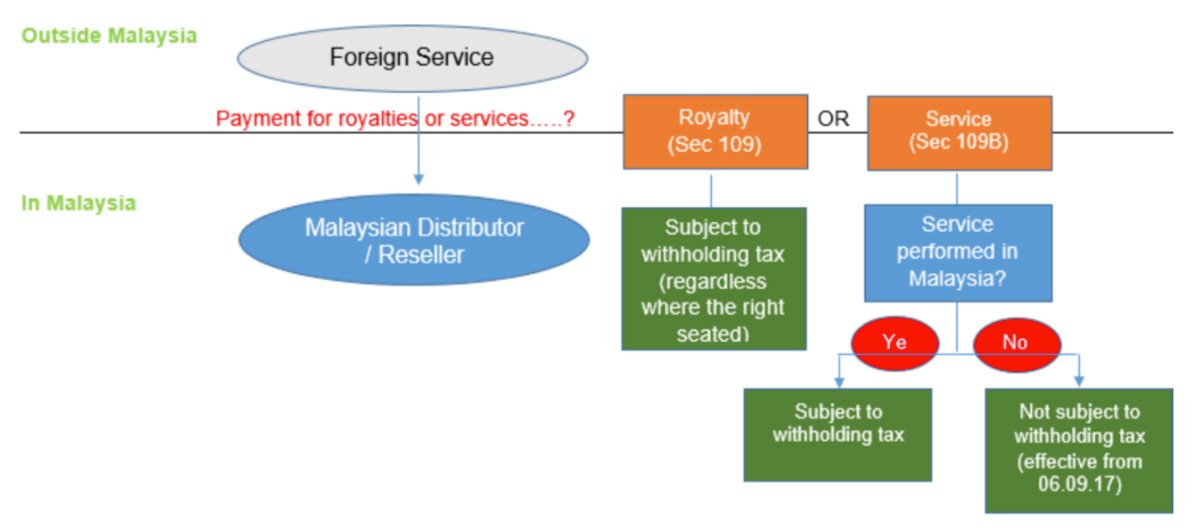

Part 2 of this article will focus on withholding tax issues around

‘royalties’ (Section 109, Income Tax Act 1967) and ‘services’ (Section

109B, Income Tax Act 1967) for e-Commerce transactions.

Any commercial transactions conducted electronically including the

provision of information, promotion, marketing, supply, order or

delivery of goods and services (even though payment and delivery

relating to such transactions may be conducted offline).

Online advertising on Facebook, online payment such as Paypal, payment for cloud computing service,

payment for subscription to content aggregators etc.