EOR Services in Malaysia: What Is an Employer of Record & How It Works

This is where Employer of Record (EOR) and Professional Employer Organisation (PEO) services play a crucial role. For companies exploring the Malaysian market, these solutions offer a compliant and efficient way to hire local talent without setting up a legal entity.

As a trusted accounting firm in Malaysia, ShineWing TY TEOH provides both PEO and EOR services that help international and regional businesses navigate local regulations, manage payroll, and ensure compliance with Malaysian employment laws.

What Is an Employer of Record (EOR)?

In simpler terms, the EOR becomes the official employer in the eyes of the law, while your business functions as the operational manager.

Key Responsibilities of an EOR in Malaysia

- Hiring and onboarding local employees.

- Managing payroll, payslips, and statutory deductions.

- Ensuring compliance with Malaysian employment law and EPF/SOCSO obligations.

- Handling income tax contributions (PCB under LHDN).

- Administering employment contracts, leave entitlements, and termination.

With EOR services, foreign companies can start operations in Malaysia quickly — without establishing a local subsidiary.

For a detailed overview of ShineWing’s offerings, visit PEO and EOR Services Malaysia.

What Is a Professional Employer Organisation (PEO)?

This approach is often used by local companies seeking to streamline HR and accounting processes or manage growing teams more effectively.

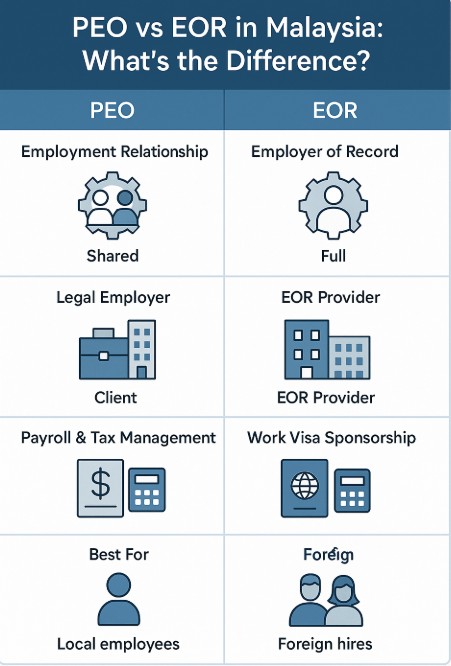

| Feature | Employer of Record (EOR) | Professional Employer Organisation (PEO) |

|---|---|---|

| Legal Employer | EOR acts as the legal employer | Client company remains legal employer |

| Entity Requirement | No local entity needed | Requires a registered local entity |

| Payroll Management | Handled by EOR | Managed jointly |

| Best for | Foreign companies entering Malaysia | Local companies optimising HR and compliance |

If you’re unsure which model suits your needs, refer to PEO & EOR Services Malaysia Guide.

How EOR Services Work in Malaysia

Understanding how an EOR functions in Malaysia helps businesses make informed decisions about market entry and workforce management.

Step 1: Onboarding & Employment Setup

The EOR drafts legally compliant employment contracts based on Malaysia’s Employment Act 1955, including statutory benefits such as annual leave, public holidays, and working hours.

Step 2: Payroll & Tax Administration

The EOR manages salary payments, statutory contributions to EPF, SOCSO, and EIS, and monthly income tax (PCB) filings under Lembaga Hasil Dalam Negeri (LHDN).

Step 3: Compliance Management

EOR providers ensure adherence to Malaysian labour regulations, including immigration rules for expatriate employees, data privacy, and termination laws.

Step 4: HR & Benefits Administration

This structure eliminates the need for a local HR department or accounting setup while maintaining compliance with Malaysian regulations.

Advantages of Using EOR Services in Malaysia

a. Quick Market Entry

Foreign companies can start operations in Malaysia within weeks, bypassing the lengthy process of establishing a legal entity.

b. Legal and Tax Compliance

EOR providers manage all statutory requirements, reducing compliance risks. This includes EPF, SOCSO, EIS, and income tax obligations.

c. Cost Efficiency

Without the need to set up a local office, businesses save on incorporation costs, administrative expenses, and staffing overheads.

d. Focus on Core Activities

EOR services allow management teams to concentrate on growth, sales, and operations — leaving payroll, HR, and compliance to local experts.

e. Local Expertise

For more on the compliance framework, visit PEO and EOR Services Malaysia: Legal Compliance.

Who Should Use EOR or PEO Services?

- Foreign companies expanding into Malaysia without a legal entity.

- Start-ups and SMEs testing new markets before full incorporation.

- Multinational corporations seeking short-term or project-based local hires.

- Companies in transition, such as mergers or acquisitions, needing temporary employment solutions.

If your organisation fits these categories, an EOR or PEO can simplify operations and reduce risk.

Key Legal Considerations for EOR and PEO in Malaysia

- EPF (Employees Provident Fund) – retirement savings.

- SOCSO (Social Security Organisation) – injury and disability protection.

- EIS (Employment Insurance System) – unemployment insurance.

Additionally, tax obligations under LHDN (Inland Revenue Board of Malaysia) apply to both local and expatriate employees.

Failure to comply can result in financial penalties or legal disputes. Partnering with an EOR ensures all documentation, reporting, and contributions meet regulatory requirements.

To learn more about Malaysian taxation, explore Company Taxes in Malaysia You Should Know.

Why Choose ShineWing TY TEOH as Your EOR Partner

a. Regional Expertise

With offices across Asia-Pacific, ShineWing TY TEOH provides international clients with consistent, compliant, and scalable HR and payroll solutions.

b. Integrated Accounting and HR Support

As a leading accounting firm in Malaysia, we offer end-to-end support — from payroll administration to financial reporting and tax advisory.

c. Strong Legal and Compliance Framework

Our team ensures adherence to Malaysian labour laws, immigration regulations, and tax requirements, minimising your compliance risks.

d. Tailored Solutions

For more on our accounting expertise, see Accounting Services in Malaysia.

PEO and EOR Services vs Outsourced Accounting

While EOR and PEO focus on employment management, outsourcing accounting functions addresses financial operations. Many businesses use both to enhance efficiency and compliance.

| Function | PEO & EOR | Outsourced Accounting |

|---|---|---|

| Primary Focus | Employment, payroll, HR compliance | Financial reporting, bookkeeping, taxation |

| Best For | Businesses expanding or hiring in Malaysia | Businesses needing finance and compliance support |

| Legal Entity | Optional (for EOR) | Required for accounting |

| Example Partner | ShineWing TY TEOH | ShineWing TY TEOH |

Discover when outsourcing finance makes sense in When to Outsource Accounting Services in Malaysia.

How EOR Services Support Business Growth

- Expand faster in new markets.

- Attract local and international talent.

- Maintain operational flexibility.

- Reduce fixed costs.

- Scale operations seamlessly across borders.

This makes EOR a strategic investment for companies pursuing long-term growth in Malaysia and the wider ASEAN region.

The Future of PEO and EOR Services in Malaysia

With increasing regulatory complexity, companies will increasingly turn to trusted digital advisory and accounting partners for integrated HR, tax, and compliance support.

To understand how these services fit into your business structure, visit PEO and EOR Services Malaysia.

Frequently Asked Questions (FAQ) About PEO and EOR Services

What is the difference between PEO and EOR services in Malaysia?

A Professional Employer Organisation (PEO) works under a co-employment model where both the client and PEO share HR responsibilities, and the client remains the legal employer. An Employer of Record (EOR), on the other hand, becomes the official legal employer in Malaysia, managing payroll, taxes, and compliance while the client oversees day-to-day work.

When should a company consider using EOR services in Malaysia?

Businesses should consider EOR services when expanding into Malaysia without a local entity, hiring short-term or remote employees, or testing the market before full incorporation. An EOR helps companies stay compliant with EPF, SOCSO, and LHDN regulations while starting operations quickly and cost-effectively.

Are EOR services compliant with Malaysian labour laws?

Yes. Reputable EOR providers, such as ShineWing TY TEOH, operate fully under the Employment Act 1955 and related regulations. They handle employment contracts, statutory contributions, and income tax compliance to ensure both the employer and employee meet legal obligations in Malaysia.

Can local Malaysian companies also benefit from PEO services?

Absolutely. Local organisations use PEO services to outsource HR and payroll functions, ensuring efficient workforce management and compliance. It’s especially valuable for SMEs that need professional HR support without maintaining an internal HR department.

Why choose ShineWing TY TEOH for PEO and EOR services in Malaysia?

ShineWing TY TEOH combines expertise in accounting, tax, and compliance with end-to-end HR management solutions. As a leading accounting firm in Malaysia, we provide integrated PEO and EOR services that simplify market entry, ensure full legal compliance, and support sustainable business expansion.

Conclusion: Simplify Market Entry with EOR Services

At ShineWing TY TEOH, we combine global expertise with local insight to deliver fully compliant, transparent, and efficient PEO and EOR solutions.

Whether you’re entering the market or optimising existing operations, our integrated accounting and HR support helps you succeed with confidence.

To explore your options, visit PEO and EOR Services Malaysia Guide.