How Imported Services Tax Affects Digital Services in Malaysia (2026 Update)

With evolving fiscal policies and expanded definitions under Malaysia’s Sales & Services Tax (SST), 2026 will be an important year for digital service providers.

Changes from Budget 2025, SST expansion, and regulatory updates solidify tighter obligations on foreign and local providers of digital/ imported services. Below is what digital businesses need to know to stay compliant as we move into 2026.

What is “Imported Services Tax” for Digital Services in Malaysia

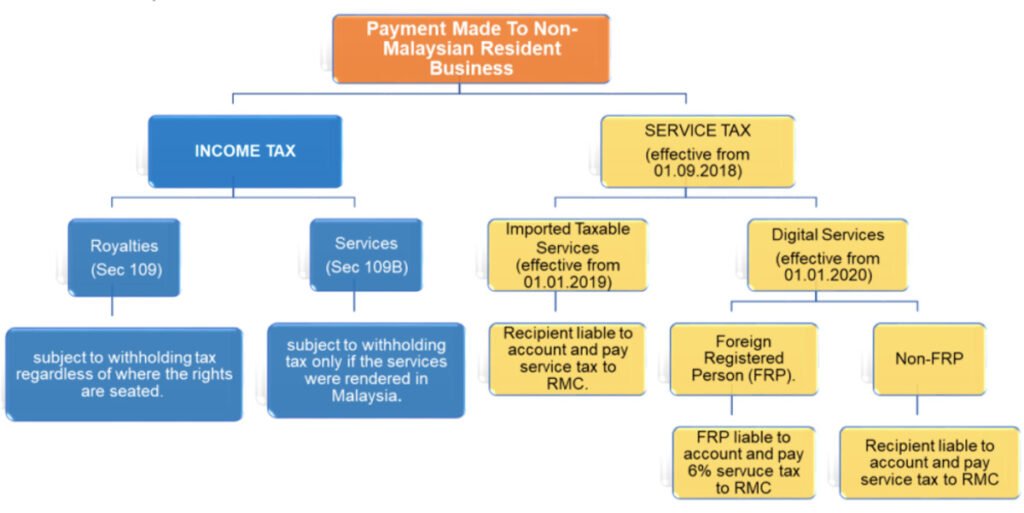

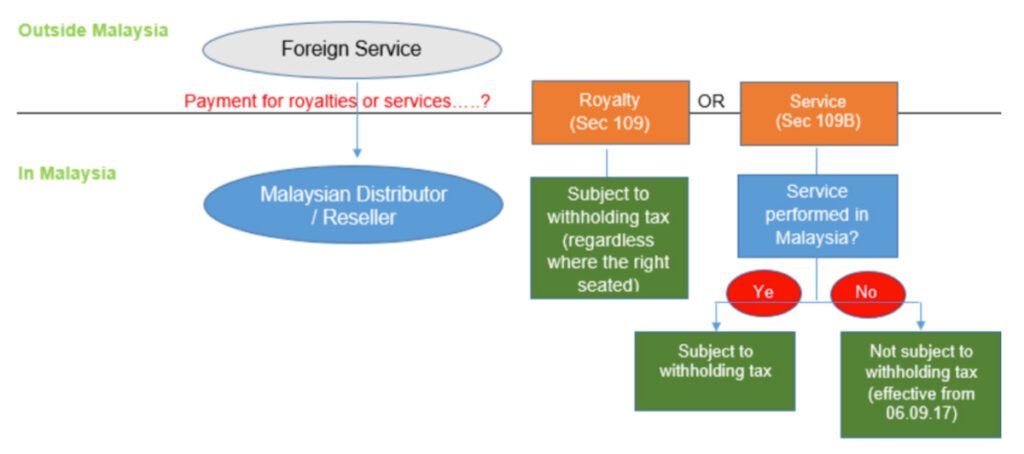

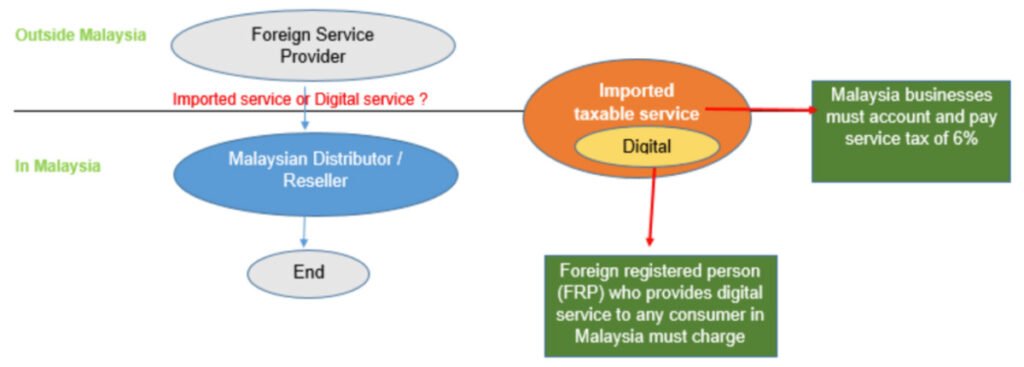

- Imported taxable services under the SST include digital services supplied by foreign service providers to Malaysian consumers or businesses. This was established under Service Tax Regulations, including amendments for Digital Services.

- These imported taxable services are subject to service tax levied by the Royal Malaysian Customs Department (RMCD).

Key Changes & Confirmed Updates as of 2025/2026

Here are the changes that have been implemented, plus those to expect or that are under discussion, affecting imported digital services:

| Change / Policy | Effective Date / Status | What It Means for Digital / Imported Services |

|---|---|---|

|

Service tax rate increase to 8% |

Took effect 1 March 2024. |

All taxable and digital services (foreign or local) generally taxed at 8%, except specified services with other arrangements. |

|

Expansion of SST service tax scope |

1 July 2025 onward. |

New service categories are included: rental/leasing of tangible assets (Group K), commercial services, etc. For digital service providers, this may bring more services under taxable definitions, depending on the nature of service. |

|

Increased registration threshold for certain services |

As part of expansion (particularly for rental / leasing services) threshold set at RM1,000,000 annual taxable turnover. |

Foreign providers or those supplying imported services must check whether their supplies to Malaysia cross that threshold, else may not need to register / charge service tax. |

|

New service categories included in taxable services |

As of 1 July 2025: rental / leasing services, commercial services, etc. |

Some digital services possibly bundled with or similar to these new categories (e.g. cloud compute tied with leasing of servers), may get captured depending on interpretation. |

|

Transitional / exemption rules |

Some transitional grace, exemption for certain contracts or non-reviewable contracts existing before expansion; exemptions for government entities etc. |

Digital providers must review their contracts, especially those spanning before/after 1 July 2025, to see how much is taxable post-expansion. |

Anticipated / Under Review Issues for 2026

While many changes have been implemented by mid-2025, moving into 2026 there are areas to watch closely — either unresolved, developing, or likely to have further clarification / regulation.

Clarification of Service Definitions

As more service types are included, there may be ambiguity for digital services that straddle categories. For example, services involving software as a service (SaaS), cloud storage, or digital platforms that include both content and functionality. The exact legal interpretation under SST / SITOD (Service Tax on Digital Services) regulations will need to be monitored.

Customer Location Rules & Proofs

For digital services, proving that a user / consumer is in Malaysia is often required to charge service tax. Rules on what constitutes sufficient proof (IP, billing address, bank card country, etc.) may be refined. Non-residents supplying might need more robust compliance processes. (Earlier digital service tax rules already required two non-conflicting pieces of data for customer location.)

Double Taxation and Withholding Interactions

Imported digital services may also attract withholding tax under other tax laws. Digital service providers and consumers must ensure that taxation is not duplicated. Previously published parts (Part 1 / Part 2 by ShineWing) discuss this interplay in detail; updates may adjust rates or treaty benefits.

Compliance / Enforcement Strengthening

Given expansion of scope, RMCD enforcement (audit, penalties) likely to be more active. Preparation for proper invoicing, tax returns, and record-keeping will become more essential. Possibly further guidance or rulings will be issued in 2026 to clarify grey areas.

Fee / Cost Impact to End Users

As service tax is applied more broadly, digital service pricing, especially B2C, may see visible cost increases unless providers absorb tax. B2B users (who are registered taxable persons) may require compliant invoices for their own accounting.

Implications for Digital Service Providers (Foreign & Local) in 2026

Based on what is known and what is likely, here are what businesses should do to stay ahead:

Review All Services Supplied

- Audit the catalogue of digital services to map which ones are clearly taxable; revisit definitions especially for mixed services.

- Check existing contracts’ terms (date spans, price revisions, location of provision) to assess exposure.

Monitor Turnover / Thresholds

- Foreign providers must track Malaysian-derived revenue carefully to see if annual turnover breaches RM1,000,000 or other thresholds.

Update Invoicing / Systems

- Ensure invoices meet SST / RMCD requirements: show service tax separately, accurate breakdown, proof of customer location where needed.

- Internal systems (billing, ERP, subscription platforms) need configuration to capture service tax where applicable.

Contractual Adjustments & Client Communication

- For services delivered across the threshold dates (pre-July 2025 vs post), ensure contracts reflect the tax obligations correctly.

- Communicate clearly to customers if service tax is applied / will be passed on, especially for B2C consumers.

Legal & Tax Advisory Engagement

- Consulting tax advisors to interpret ambiguous cases.

- Keep abreast of RMCD / MOF / legislative guidance / regulatory clarifications issued in 2026.

Documentation & Record-Keeping

- Maintain records (invoices, payment receipts, customer data) for required number of years as per regulation.

- Be able to substantiate customer location for digital transactions.

Potential Risks if Ignored

- Unintentional non-compliance → penalties, back taxes, possible reputational risk.

- Mispricing: absorbing unexpected service tax or passing it poorly to customers → margin erosion or customer dissatisfaction.

- Contract disputes: if service tax was not accounted for in deals spanning effective dates, or where customers expected digital services to be tax-exempt but are not.

- Audit exposure: because SST expansion is a revenue priority for the government, enforcement will likely tighten.

What Clients / Businesses Should Watch in 2026

- Any MOF / RMCD announcements clarifying new digital service tax definitions.

- Cases (court or administrative) that set precedent for what counts as “imported service” or “digital service”.

- Treaty changes or updates that may affect withholding tax implications.

- Software / platform changes: e.g. if platform providers decide to absorb tax or include tax in pricing.

- Technology compliance changes: new ways RMCD wants proof of location, electronic invoicing, data privacy implications for gathering proof etc.

Frequently Asked Questions (FAQ) on Imported Services Tax in Malaysia (2026)

As of 2026, most imported taxable services, including digital services, are subject to 8% service tax. Certain categories (e.g., F&B, telecom, parking, logistics) remain at 6%.

Foreign service providers supplying taxable digital services to Malaysian customers must register with the Royal Malaysian Customs Department (RMCD) if their annual revenue from Malaysia exceeds RM1 million.

Digital services include software subscriptions (SaaS), cloud hosting, online advertising, streaming, mobile apps, and other services delivered over the internet by foreign providers.

Yes. If the foreign provider is registered with RMCD, they will charge service tax. If not, Malaysian businesses may be required to self-account for service tax on imported services.

- Service tax applies to the consumption of digital/imported services (indirect tax).

- Withholding tax applies to certain payments to non-residents for services, royalties, or interest (direct tax under the Income Tax Act 1967).

In some cases, both may apply.

If the provider is registered with RMCD, they will add 8% service tax to the invoice. Your business must account for that in its expenses.

Yes, certain services are exempt (e.g., residential rental, financial leases, reading materials). Transitional rules also apply for contracts signed before 1 July 2025 that extend into 2026.

Foreign providers must rely on at least two non-conflicting pieces of evidence (e.g., billing address, payment card country, IP address) to confirm a Malaysian customer.

Conclusion

As Malaysia moves into 2026, the SST landscape for imported and digital services is no longer speculative—it’s being enforced with broader reach.

The jump to 8% for service tax, the inclusion of many new service categories, and higher registration thresholds mean that even services previously thought outside the SST net may now be taxable.

For digital service providers (both foreign and domestic), remaining proactive—reviewing services, strengthening compliance systems, and staying informed of forthcoming regulations—will be critical. Those who prepare in 2025 will be much better placed to avoid surprises in 2026.