3

200,000

100,000

2

100,000

2

2

100,000

100,000

3

200,000

3

2 per group

3 per group

4 per group

Increase of 1 employee for every additional 10 related companies or Labuan Islamic leasing companies;

100,000 for each Labuan leasing company or Labuan Islamic leasing companies;

100,000 for each Labuan leasing company or Labuan Islamic leasing companies;

100,000 for each Labuan leasing company or Labuan Islamic leasing companies;

100,000 for each Labuan leasing company or Labuan Islamic leasing companies;

2

2

100,000

2

2

100,000

2

2

100,000

2

2

100,000

2

100,000

2

120,000

2

2

50,000

1

20,000

20,000

Income derived from intellectual property rights is subject to tax at the rate of 17% or 24% under Income Tax Acts 1967(“ITA”)

With effect from 1 Jan 2019, under Income Tax (Deductions Not Allowed for Payment Made to Labuan Company by Resident) Rules 2018 (Amendment) 2020, the following type of payments made to a Labuan Entity by a company resident in Malaysia are not entitled to a tax deduction:

No service tax shall be charged on any taxable service provided within or between Special Areas and Designated Areas unless on the taxable services prescribed in the Service Tax (Imposition of Tax for Taxable Service in Respect of Designated Areas and Special Areas) Order 2018.

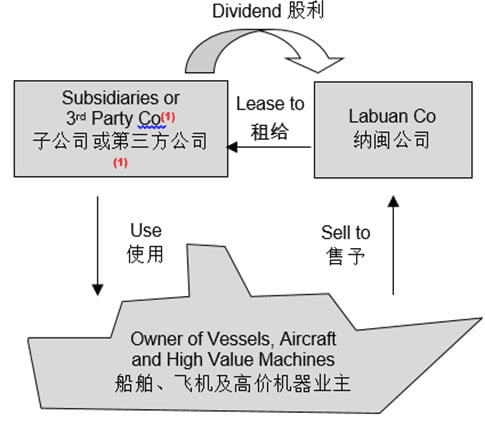

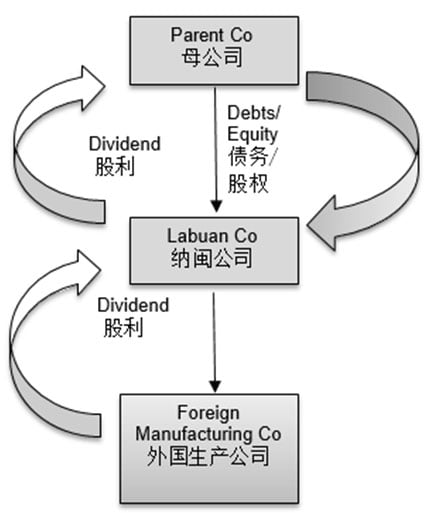

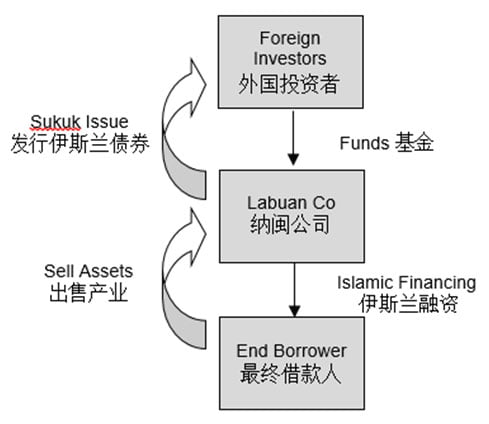

There is no withholding tax on dividends paid by a Labuan Company in respect of dividends distributed out of income derived from Labuan business activities or income exempt from income tax. Interest, royalties, lease rental, technical fee and management fees paid to a non- resident are not subject to withholding tax.

Certain home country may impose the income tax law on incomes deriving from offshore, if they have not been taxed offshore, particularly, when they are remitted back, this may appy to BVI Co but not Labuan Co as it pays minimum tax.

BVI enjoys only 2 countries’ (Japan and Switzerland) double tax treaties (DTAs), and these treaties are not used in practise.

Dividend declared from Labuan Co to Malaysia is free of tax.

Note: If the company is Non-Malaysian Co, the tax exemption will depend on each home country’s law jurisdiction and its double tax treaties with Malaysia.

No withholding tax on interest payment.

BVI has applied the European Union (EU) Savings Directive since 1 July 2005. A withholding tax (initially 15%, rising to 20% from 1 July 2008) has been applied to interest payments to natural persons resident within the EU.

Labuan has its registered auditor under its jurisdiction. The income tax payable is allowed to base on the audited profit, the source of income is cleared for reinvestment or dividend purpose, once it is paid.

BVI has no registered auditor under its jurisdiction.

Suitable Industries

Tax Advantages

Suitable Industries :

Tax Advantages

Suitable Industries :

Tax Advantages

Income tax is only 3% of net profit

Suitable Industries :

Tax Advantages

Other Advantages

Incentive Commitment

| Labuan Entities | Annual operating expenditures |

|---|---|

Labuan International

Commodity Trading

Company.

|

RM3,000,000 (USD 750,000) per entity in Malaysia

(including minimum of RM100,000 (USD 25,000) in

Labuan). RM3,000,000 (USD 750,000) per entity in Malaysia (including minimum of RM100,000 (USD 25,000) in Labuan). Local business spending including:

|

| Labuan Entities | Minimum number of full time employees in Labuan |

|---|---|

Labuan International

Commodity Trading

Company.

|

2 staff per group. Increase of 1 employee for every additional 5 LITC companies. |

c. To employ at least three (3) professional traders who are tax residents of Malaysia.

Operational Requirements

Requirements

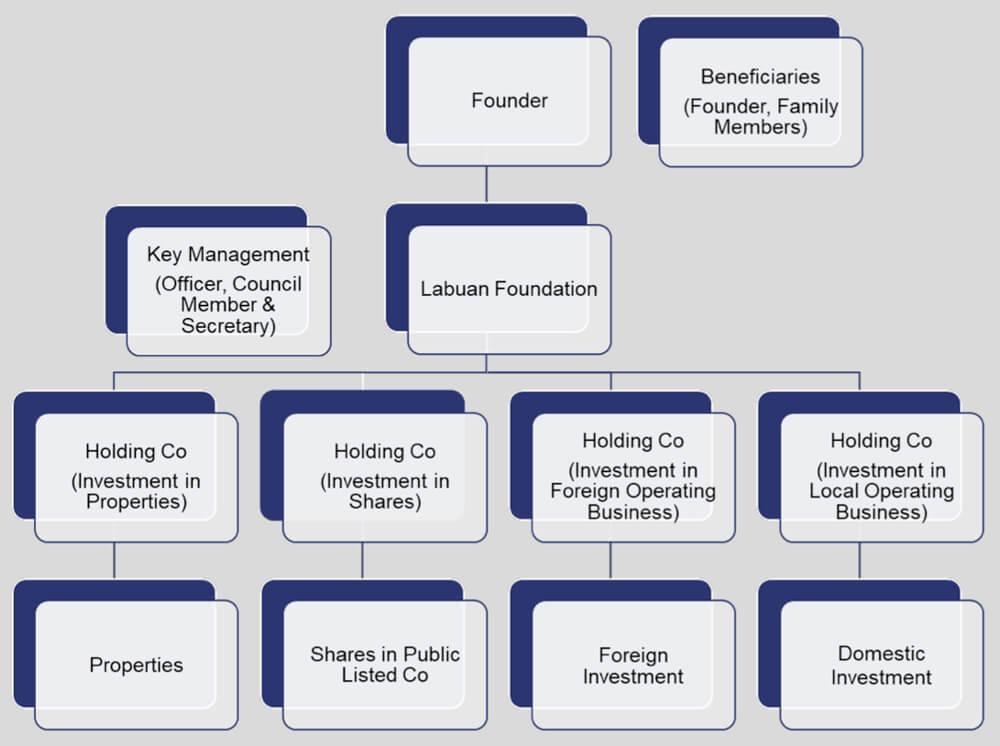

Labuan Foundation is probably one of the Best Choices in Asia as your wealth management vehicle. While there are 21 jurisdictions worldwide which have Foundation Acts to govern wealth management activities, Labuan which is governed by the Labuan Foundation Act 2010, remains the ONLY jurisdiction in Asia. As such, your assets are protected under its own jurisdiction from the local or foreign claims and cannot be liquidated forcefully.

Labuan Foundation has other Silent Features as private wealth management vehicle as below:

Control

Confidentiality

End beneficiaries is anonymous.

Capital Transfer

No capital requirements. Minimum endowment of USD1.00 as an initial asset at time of establishment.

Nationality

No requirement for founder/councillor.

Appeal Against Transfer By Creditors

Only within the first two years of registration.

Appeal Against Inheritance Provisions

No appeal possible because of foreign laws.

Foreign Claim Or Judgment

Unenforceable

Rights And Powers Of A Founder

Enshrined via the charters.

Holding Of Malaysian Assets For Non-charitable Foundations

May hold with Labuan FSA’s approval.

Involvement Of Corporate Body

Allowed to be appointed as :

Duration

Fixed or perpetual.

Dissolution

Assets returned to designated party.

Ownership Of Foundation’s Asset

Beneficiary has no legal or beneficiary ownership over the foundation’s asset.

Taxation On Income

Whether you’re targeting Hong Kong, Singapore, or a global stock exchange, our Pre-IPO Advisory helps you prepare with confidence. From strategic planning to post-listing compliance, ShineWing TY TEOH ensures a smooth transition to public markets.

We provide strategic and technical support to prepare your company for public listing:

| Area | Key Services |

|---|---|

|

Corporate Readiness |

IPO structure planning, internal control review, governance setup |

|

Financial Advisory |

Financial due diligence, IFRS compliance, audit readiness

|

|

Valuation & Tax |

Pre-IPO valuation, tax optimization, group restructuring |

|

Investor Preparation |

Pitch materials, analyst briefings, investor Q&A training

|

Identifies gaps and risks early in the process

Improves company valuation and investor trust

Ensures compliance with regional and global stock exchange requirements

Builds strong internal controls and corporate governance practices

Positions your business for long-term growth post-IPO

| Phase | What We Offer |

|---|---|

|

Pre-IPO |

IPO roadmap, gap analysis, board composition, ESG advisory

|

|

IPO Execution |

Liaison with legal/accounting/tax parties, prospectus review, due diligence

|

|

Post-IPO |

Ongoing compliance, investor relations support, financial reporting

|

| Before Listing | During Listing |

|---|---|

|

Determine the proposed listing business or scope of the entity. |

Form an internal team responsible for listing. |

|

Plan for restructuring of the listing group. |

Appoint external professional parties. |

|

Introduce strategic investors. |

Prepare and submit listing documents. |

|

Decide to go listed or seek other forms of fund raising. |

Respond to questions raised by SEHK regarding the listing documents. |

|

Estimate the amount of funds raised through listing. |

Attend listing hearings and get the approval for listing from the Listing Committee. |

|

Determine the proposed listing business or scope of the entity. |

Form an internal team responsible for listing. |

|

Plan for restructuring of the listing group. |

Appoint external professional parties. |

|

– |

Arrange press conference and roadshow. |

|

– |

Issue prospectus. |

Upon listed, the listed company must strictly comply with the Securities and futures Ordinance and the Listing Rules to provide the public with accurate information on timely basis. The major requirements include:

Pre IPO Advisory refers to the strategic and technical support provided to companies before they go public. It includes financial readiness, governance restructuring, compliance checks, valuation, and investor preparation — ensuring the company is fully prepared for listing.

Without proper preparation, companies risk delays, compliance issues, or lower valuations during the IPO process. Pre IPO Advisory helps identify gaps early, improves investor confidence, and ensures a smoother transition to public markets.

Ideally, companies should begin 2–3 years before listing to allow sufficient time for corporate restructuring, internal control reviews, and regulatory compliance. However, the timeline may vary depending on the company’s size and market readiness.

Depending on jurisdiction and complexity, timelines range from 12 to 24 months.

Any company considering going public — from family-owned businesses to multinational corporations — can benefit from Pre IPO Advisory. It is especially important for companies seeking to expand regionally or globally.

Costs vary based on the complexity of the listing, market requirements, and scope of services. Typical expenses include legal, audit, sponsor, regulatory, and advisory fees. ShineWing TY TEOH provides tailored guidance to help businesses plan their IPO budget effectively.

It depends on your business model, investor target, and growth goals. We help assess fit.

Note:

For the Listing Criteria and Requirements on Hong Kong Stock Exchange, Singapore Stock Exchange, NYSE, NASDAQ, OTC, Australia Stock Exchange, London Stock Exchange, Borse Frankfurt Stock Exchange and Taiwan Stock Exchange, please refer to PDF.

In a bid to enhance the quality of Halal parks and make them more fascinating, certain incentives are recommended, they include:

The Northern Corridor Economic Region (NCER) is a development plan encompassing the four Northern States of Malaysia namely Perlis, Kedah, Perak and Penang. The priority sectors in NCER are manufacturing, agriculture and bio-industries and services which include the sub-sectors of tourism, global business services and logistics & connectivity.

The objectives of the NCER initiative include:

a) To stimulate economic growth to address the imbalances and increase inclusively;

b) To achieve balance growth in the manufacturing, agriculture, bio-industries and services sectors;

c) To enhance talents to meet the growing needs of the region;

d) Increase private sector investments and finance initiatives.

The advantages include:

a) Located within the Indonesia-Malaysia-Thailand Growth Triangle (IMT-GT);

b) NCER has hosted many multinational companies and local companies with approximately RM47.7 billion of investment in the year 2009 – 2016;

c) Year 2020, RM50 million for high impact strategic projects has been allocated to Chuping Valley Industrial Area in Perlis;

d) NCER plays a predominant role in agriculture in the NCER;

e) NCER is renowned for its rich natural and heritage attraction.

An inland port to capitalize on the border trade from southern Thailand.

An on-going industrial park development to transform Perlis into an industrialised state.

A new industrial park that focuses on science and technology clusters located at the border region.

Project that will focus on downstream rubber activities by creating a complete rubber.

A. Manufacturing

1. Electrical & Electronic

2. Machinery & Equipment

a. Green Technology (product)

b. Medical Devices (products)

c. Automotive (products)

d. Additive Manufacturing (products)

e. Aerospace (products)

B. Agriculture & Bio-Industries

a. Sustainable Agriculture

b. Processing of Agriculture Produce

c. Superfruit/ Superfood (Upstream)

d. Superfruit/ Superfood (Downstream)

e. Green Technology Services

f. Halal Industry Seed Research & Development

D. Medical Science and Science & Technology

In-House R&D

Research & development undertaken by Malaysian company for their own business.

R&D Company

Research on science or technology including Industry 4.0 for the production/ improvement of materials, equipment, products or processes.

Seed R&D Centre

Investor

Seed R&D Centre

Operator

Approved Agriculture Project

Education

a. Private Institution of Higher Learning

b. Technical & Vocational Education and Training (TVET)

c. International/ Private Schools

1. KSTP Park Manager

4. KSTP Global Research Centre (GRC)

Income tax exemption of 100% of statutory income for 15 years (5+5+5).

1. Income tax exemption of 70% of statutory income for 5 years for the following income:

a. Disposal of all or part of right or land/building located at CVIA; OR

b. Rental of all or part or the land/buildings located at CVIA.

2. Stamp duty exemption on transfer or lease of land only.

Income tax exemption of 100% of statutory income for 5 years.

3. Waste-To-Resources Facilities Provider

1. Manufacturer

3. Main Developer and Residential and Commercial Developer

Promoted Activity

ECER Incentives

Promoted Activity

ECER Incentives

Tourism

Promoted Activity

ECER Incentives

Culture and Heritage

Promoted Activity

ECER Incentives

Agriculture

Promoted Activity

ECER Incentives

Agriculture – related services

Promoted Activity

ECER Incentives

Promoted Activity

ECER Incentives

Promoted Activity

ECER Incentives

Income tax exemption for 10 years commencing from the year company derives statutory income:-

2. Approved development manager providing management, supervisory or marketing services in relation to the development of an industrial park or free zone.

3. Approved park managers providing park management services including maintenance, marketing and rental of common facilities and utilities services in the industrial park or free zone.

Income tax exemption for 10 years commencing from the year company derives statutory income derived from a qualifying activity.

4. Qualifying person who sponsors a hallmark event.

A deduction equivalent to the amount not exceeding RM1 million for each year of assessment in respect of cash contribution or contribution-in-kind.

To minimise the risks associated with the accounting and tax issues of the transactions, ShineWing performs in-depth due diligence.

Financial Position

Tax Position

Risk Control

Commercial due diligence focuses on conducting extensive and in-depth analysis of the target and collecting opinions from industry experts.

Market and Regulatory Environment

Suppliers and Customers

Competitors

Target

Over the years, our professional teams have accumulated a wealth of experience in different industries. We can provide all-round support throughout the transaction for clients spanning a range of sectors all over the world, focusing on the unique characteristics and needs of each industry.

The areas where ShineWing has been involved in cross-border M&A deals:

North America

South America

Europe

Africa

ShineWing has over 7,000 professionals worldwide. Leveraging the resources of our member firms, our professional teams have in-depth M&A knowledge, with a good understanding of different local markets as well as global vision, offering genuinely international services to our clients.

ShineWing was named as one of the Top 20 global accounting networks and had been awarded the Rising Star Network by the International Accounting Bulletin (IAB). ShineWing is also widely recognised by statutory and professional institutions. We have offices in at least 24 major cities in China. ShineWing is the leading professional services provider in Asia Pacific.

ShineWing is a member of Praxity, which has participating firms in over 100 countries operating out of over 690 offices globally. We work closely with Praxity to provide comprehensive international M&A advisory services. We can cater to the needs of clients at different stages, ranging from searching for M&A targets to providing due diligence and tax advisory services.

One Belt one Road (“The Silk Road Economic Belt and The 21st century Maritime Silk Road”) initiated by the People of Republic China’s Government in 2013 and was to focus on creating networks for more efficient and productive free flow of trade as well as the integration of international markets both physically and digitally.

The initiative includes six international corridors:

ShineWing China Practice established in the early 1980s with HQ located in Beijing and has expanded across in the major cities of China, including Shenzhen, Chengdu, Shanghai, Xi’an, Tianjin, Qingdao, Changsha, Changchun, Yinchuan, Jinan, Dalian, Kunming, Guangzhou, Fuzhou, Nanjing, Urumqi, Wuhan, Hangzhou, Taiyuan, Chongqing, Nanning and Hefe.

ShineWing China is a registered auditor of public interest entities trade on two China Stock Exchange, the Shanghai Stock Exchange and the Shenzhen Stock Exchange including A-Shares, B-Shares and H-Shares and served more than 240 public listed companies in China including China State-owned enterprises, Fortunate 500 and multi-national corporations.

Today, ShineWing International has been established as a global network of independent accounting and consulting firms, ShineWing member firms communicate and work with one another closely being part of ShineWing network, and with the leverage of our China team’s expertise, experiences, network and geographical presence in China, no matter which part of China you are located, ShineWing TY TEOH helps China business venture into Malaysia without hassle-free experiences.

China One Belt One Road Businesses venture into Malaysia have engaged us for ongoing work or specific projects. Client Reference are available upon request.

Corporate Member of TheInstitute of Internal Auditors (IIA)

Approved and registered under Accounting Oversight Board (PCAOB)

Approved Auditor of Labuan Financial Services Authority (Labuan FSA)

Awarded as Top 20 largest international accounting network by International

Accounting Bulletin.

Marketing-related:

Trademarks, trade names, service marks, collective marks, certification marks, internet domain names, trade dress and newspaper mastheads.

Customer-related:

Customer lists, order or production backlog, customer contracts and the related customer relationships which meet contractual criterion, and non-contractual customer relationships which meet the separability criterion.

Artistic-related:

Plays, operas, ballets, books, magazines, newspapers, literary works, video and audio-visual materials, musical works, pictures and photographs and artistic works which meet contractual criterion.

Contract-based:

Licences, royalties and standstill agreements, advertising, construction, management, service or supply contracts, lease agreements, franchises, operating and broadcasting rights, use rights such as drilling, water, air, mineral and timber-cutting, servicing contracts such as mortgage and employment contracts and non-competition agreements.

Technology-based:

Patented and non-patented technology, computer software, mask works, databases and trade secrets such as formulas, process or recipes.

For financial perspective

For marketing perspective

For legal perspective

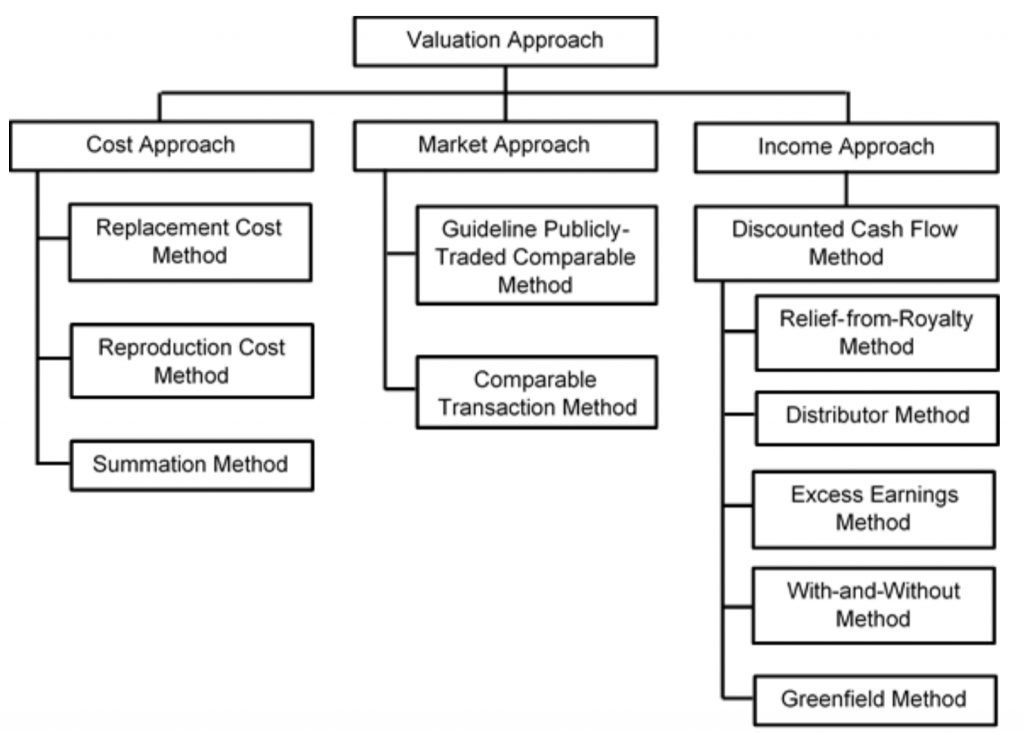

Cost approach is a general way of determining a value indication of a business, business ownership interest, or security using one or more methods based on the value of the assets net of liabilities.

In the valuation of a business, cost approach presents the value of all the tangible and intangible assets and liabilities of the company.

Based on the principle of competition, market approach assumes if one thing is similar to another and could be substituted for the other, they would compete with each other, then they must be equal in value. The fair value derived must be based on a sufficient number of comparable companies / market transactions in order to derive a relevant and meaningful comparison.